%20(63).png)

The Nexperia Seizure: Europe's Watershed Moment in the Global Semiconductor War

How a 73-year-old law and a Dutch chipmaker became ground zero in the battle for technological sovereignty

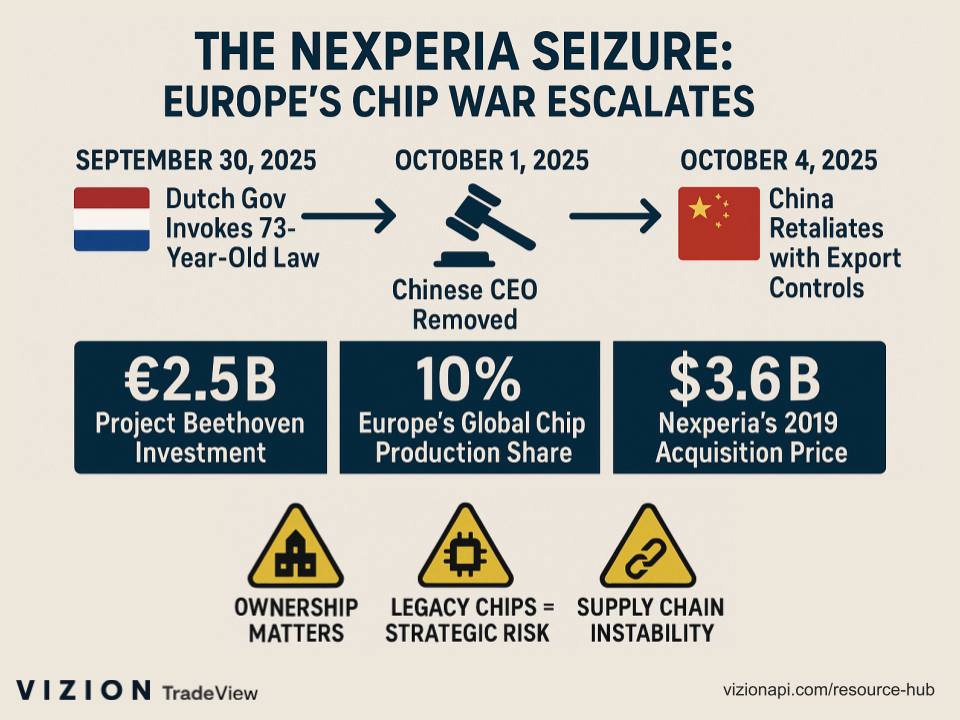

On September 30, 2025, the Netherlands crossed a technological Rubicon. In an unprecedented move that reverberated across global supply chains, the Dutch government invoked the never-before-used Goods Availability Act—a 73-year-old law gathering dust since the height of the Cold War—to wrest control of Nexperia, a Chinese-owned semiconductor manufacturer headquartered in Nijmegen. One week later, an Amsterdam business court suspended the company's Chinese CEO, Zhang Xuezheng, replacing him with a Dutch interim chief.

This wasn't merely a regulatory action. It was Europe's most aggressive assertion yet that the age of passive acceptance of Chinese control over strategic technology assets has ended.

A Company Caught in the Crossfire

Nexperia's story encapsulates the tangled realities of modern semiconductor geopolitics. Once part of Dutch electronics giant Philips, the company was acquired in 2019 by Wingtech Technology, a Chinese conglomerate controlled by entrepreneur Zhang Xuezheng, for $3.63 billion. The company manufactures legacy chips—the unglamorous but essential semiconductors that power everything from automotive systems to consumer electronics. These aren't the cutting-edge processors grabbing headlines in the AI race; they're the foundational components that make modern life function.

With manufacturing facilities spanning Britain and Germany, assembly operations in China, the Philippines, and Malaysia, and thousands of employees across continents, Nexperia represents the quintessential globalized supply chain. Yet this very interconnectedness has become its vulnerability as geopolitical fault lines harden.

The Dutch intervention stemmed from mounting evidence that Zhang was allegedly undermining Nexperia to benefit his privately-owned Chinese ventures. According to reports, Zhang had forced Nexperia to place orders with WingSkySemi, his personal chip factory in China, diverting resources and potentially technology from the Dutch operation. Combined with Wingtech's placement on the U.S. Entity List in December 2024 for allegedly aiding China's efforts to acquire sensitive semiconductor manufacturing capabilities, the situation had become untenable for Dutch authorities.

The American Shadow

While Dutch officials insist their decision was made independently, court documents reveal a more complex picture. In June 2025, U.S. Department of Commerce officials told the Dutch Ministry of Foreign Affairs that Nexperia could face sanctions unless the company replaced its Chinese CEO. "The fact that the company's C.E.O. is still the same Chinese owner is problematic," American officials stated bluntly.

The timing is hardly coincidental. Just hours before the Dutch invoked the Goods Availability Act, the United States expanded its trade blacklist to include additional Nexperia entities. The message was clear: in the semiconductor domain, there's no neutral ground between Washington and Beijing.

This represents a fundamental shift in transatlantic relations. The Netherlands, home to ASML—the world's only manufacturer of extreme ultraviolet lithography machines essential for advanced chipmaking—finds itself at the epicenter of technology competition. The U.S. has long pressured the Dutch to restrict ASML's sales to China. Now that pressure extends to preventing Chinese control of any significant semiconductor assets on European soil, regardless of how "legacy" the technology might be.

China's Swift Retaliation

Beijing's response was immediate and forceful. On October 4, just days after the Dutch action, China's Ministry of Commerce imposed export controls prohibiting Nexperia's Chinese subsidiaries and subcontractors from exporting products manufactured in China. In a darkly symmetrical move, China deployed the same national security justifications that Western governments have increasingly wielded against Chinese companies.

The situation escalated further when Nexperia's Chinese operations reportedly told employees to ignore directives from Dutch headquarters—effectively a corporate insurrection backed by state authority. Zhang Xuezheng, though suspended from his CEO position, allegedly continued issuing instructions to Chinese staff, creating a bifurcated company operating under competing command structures.

Chinese Ministry of Commerce spokesperson He Yongqian characterized the Dutch government's takeover as "a clear example of how the American rule harms the legitimate rights and interests of Chinese companies." Wingtech, for its part, called the intervention "excessive interference driven by geopolitical bias" and accused non-Chinese Nexperia executives of attempting a "cloaked power grab."

The irony is thick. For years, Western companies entering the Chinese market faced mandatory technology transfers and forced joint ventures—precisely the practices China now condemns when the tables are turned.

The Broader European Awakening

The Nexperia seizure represents just one front in Europe's belated recognition of its semiconductor vulnerabilities. The continent that once dominated electronics manufacturing has watched its global chip production share decline dramatically. Today, Europe accounts for less than 10% of global semiconductor production, while depending heavily on Asian suppliers—and increasingly, Chinese manufacturers of legacy chips.

This dependency crystallized painfully during the COVID-19 pandemic when chip shortages paralyzed European automotive production. Car manufacturers, accustomed to just-in-time supply chains, discovered that $50,000 vehicles sat idle on factory floors for want of $5 chips. The wake-up call spurred action.

Project Beethoven, launched by the Netherlands in March 2024, allocates €2.51 billion to strengthen the Dutch chip industry, with a particular focus on the Brainport Eindhoven hub—the innovation ecosystem surrounding ASML. The initiative concentrates on three pillars: talent development through investment in technical education and attraction of international knowledge workers; smart infrastructure to improve accessibility and digital networks; and R&D support for semiconductor innovation. Government.nl

But Project Beethoven alone won't solve Europe's semiconductor sovereignty challenge. The EU Chips Act aims to double Europe's global semiconductor market share to 20% by 2030, but critics argue it lacks coherent long-term strategy, amounting to a "collection of ideas and initiatives" rather than a unified industrial policy.

The Technology Transfer Gambit

Perhaps most provocatively, the European Union is now considering turning China's own playbook against it. EU Trade Commissioner Maros Šefčovič recently floated the idea of requiring Chinese firms seeking to invest in Europe to transfer technology to European companies—the exact practice Western businesses have long complained about in China.

"If we invite Chinese investments to Europe, it must come with the precondition that we also have some kind of technology transfer," Šefčovič stated following an EU trade ministers meeting. The measures would apply to companies seeking access to key digital and manufacturing markets like automobiles and batteries, potentially requiring firms to use EU goods and labor, add value on EU soil, and possibly form joint ventures with European partners. Yahoo Finance

While technically applicable to all non-EU firms, the policy's target is unmistakable: countering China's manufacturing dominance before it becomes irreversible. The EU finds itself caught between principle and pragmatism. Having long criticized China's forced technology transfer requirements as violations of free trade norms, Europe now contemplates adopting similar measures to protect its industrial base.

Strategic Implications for Global Supply Chains

The Nexperia affair illuminates several uncomfortable truths about the emerging technological order:

- The Myth of Neutral Ground: Companies operating in strategic sectors can no longer maintain the fiction of being apolitical commercial entities. Geographic headquarters, ownership structures, and management nationality have become determinative factors in their operational freedom. The global supply chain, optimized over decades for efficiency, now faces fragmentation along geopolitical lines.

- Legacy Chips Matter: While cutting-edge AI processors capture headlines, the Nexperia case underscores that technological sovereignty extends to seemingly mundane components. A nation dependent on foreign suppliers for basic chips is as vulnerable as one lacking advanced processors—perhaps more so, given the ubiquity of legacy semiconductors across critical infrastructure.

- The Clawback Era: As Rhodium Group's Reva Goujon noted, governments worldwide are working to "claw back" strategic assets previously sold to Chinese entities. The Nexperia seizure likely represents the beginning, not the apex, of this trend. Expect similar actions across Europe and allied nations as the realization sets in that past transactions may have traded short-term capital for long-term vulnerability.

- Supply Chain Weaponization: China's immediate export controls on Nexperia demonstrate that supply chains have become offensive weapons, not merely objects of protection. Each side possesses leverage at different points in the value chain, creating mutual vulnerability. The semiconductor industry, built on hyper-specialization and global integration, faces potential fracture into competing technological blocs.

- The Autonomy Paradox: Europe's quest for "strategic autonomy" collides with the reality of American influence. The Netherlands acts to protect its semiconductor industry, yet does so partly at American behest. True autonomy would mean making decisions that might displease both Washington and Beijing—a position few European nations appear willing or able to adopt.

Nexperia Supply Chain Map

Nexperia is a global semiconductor manufacturer headquartered in Nijmegen, Netherlands (Chinese-owned by Wingtech Technology), producing essential semiconductors including discretes, MOSFETs, diodes, transistors, ESD protection devices, GaN FETs, and logic ICs. The company ships over 100 billion units annually with approximately $2 billion in revenue.

Here's a comprehensive breakdown of Nexperia's supply chain organized by tier levels and freight types:

TIER 1 SUPPLIERS (Direct Suppliers to Nexperia)

Raw Materials & Wafer Suppliers

- Shin-Etsu Chemical Co., Ltd. (Japan) - Silicon wafers

- SUMCO Corporation (Japan) - Silicon wafers

- GlobalWafers Co., Ltd. (Taiwan) - Silicon wafers

- Siltronic AG (Germany) - Silicon wafers

- SK Siltron (South Korea) - Silicon wafers

Note: Nexperia's 2024 Sustainability Report confirms they procure high-quality raw silicon wafers from "a select few suppliers with whom we maintain strong relationships."

Packaging Materials & Lead Frame Suppliers

- Mitsui High-tec, Inc. (Japan) - Lead frames

- Shinko Electric Industries Co., Ltd. (Japan) - Lead frames

- Dai Nippon Printing (DNP) (Japan) - Lead frames and packaging materials

- Chang Wah Technology (Taiwan) - Lead frames

- ASM Pacific Technology (Hong Kong) - Assembly equipment and materials

Chemical & Specialty Materials

- Various specialty chemical suppliers for plating materials, etching compounds, and packaging compounds (specific suppliers not publicly disclosed)

TIER 2 SUPPLIERS (Suppliers to Tier 1)

Raw Silicon & Polysilicon Providers

- Hemlock Semiconductor (USA) - Polysilicon

- Wacker Chemie (Germany) - Polysilicon

- REC Silicon (Norway) - Polysilicon

Metal & Substrate Suppliers

- Copper alloy suppliers for lead frame production

- Gold/silver plating material suppliers

- Specialty metal providers for semiconductor packaging

Equipment & Tooling Suppliers

- Semiconductor manufacturing equipment suppliers

- Precision tooling manufacturers for lead frame stamping

- Testing and inspection equipment providers

NEXPERIA'S MANUFACTURING FACILITIES

Front-End (Wafer Fabrication)

- Hamburg, Germany - Main wafer fab (200mm + WBG semiconductors)

- Manchester, UK - Power MOSFETs wafer fab (200mm)

- Shanghai, China - 300mm wafer fab (newer facility, ramped in 2024)

Back-End (Assembly & Test)

- Dongguan (Guangdong), China - LARGEST assembly site (70% of total end-product capacity)

- Seremban, Malaysia - Assembly center

- Cabuyao, Philippines - Assembly center

- Wuxi, China - Assembly center (currently in installation phase)

Critical Note: Approximately 80% of Nexperia's total end-product capacity resides in mainland China

TIER 1 CUSTOMERS (Companies that purchase from Nexperia)

Automotive Tier 1 Suppliers

- Bosch (Germany) - Electronics and control systems

- Continental (Germany) - Automotive electronics

- DENSO (Japan) - Automotive components

- ZF Friedrichshafen (Germany) - Automotive systems

Electronics Manufacturing Services (EMS)

- Foxconn (Taiwan/China)

- Flex (Singapore)

- Jabil (USA)

- Celestica (Canada)

- Pegatron (Taiwan)

- Sanmina (USA)

- Quanta (Taiwan)

Authorized Distributors (56.1% of revenue)

- Arrow Electronics (USA)

- Avnet (USA)

- Future Electronics (Canada)

- WPI Group (Taiwan)

OEM Customers (39.7% of revenue)

Direct automotive manufacturers including:

- Volkswagen Group (Germany)

- BMW (Germany)

- Mercedes-Benz (Germany)

- LG Electronics (South Korea)

- Various consumer electronics manufacturers

FREIGHT & LOGISTICS BREAKDOWN

OCEAN FREIGHT (Primary Mode - ~60-70% of volume)

- Asia to Europe

- Dongguan/Shanghai → Hamburg/Rotterdam ports

- Used for: Finished products from China assembly to European distribution

- Typical transit: 30-40 days

- Asia to Americas

- Dongguan/Shanghai → Los Angeles/Long Beach/New York ports

- Used for: Finished semiconductor products

- Typical transit: 14-30 days

- Intra-Asia

- China → Malaysia → Philippines (between assembly sites)

- Used for: Semi-finished goods, wafer transfers

Container Types:

- Temperature-controlled containers (semiconductors require climate control)

- Standard 20ft/40ft containers with specialized packaging

- High-value cargo handling procedures

AIR FREIGHT (Express/Time-Critical - ~20-30% of volume)

- Europe to Asia

- Hamburg → Shanghai/Hong Kong/Singapore

- Used for: High-value wafers from Germany fabs to China assembly

- China to Global Distribution

- Shanghai/Guangzhou → Frankfurt/Amsterdam/Chicago/Dallas

- Used for: Rush orders, new product launches, shortage management

- Intra-Regional Express

- China → Japan/Korea/Taiwan (customer deliveries)

- Europe regional distribution

Characteristics:

- 1-5 day delivery windows

- Premium pricing (3-5x ocean freight)

- Used for high-value products and emergency shipments

- Sub-6 hour latency updates critical for automotive supply chains

Likely Air Freight Partners (based on semiconductor industry standards):

- DHL Express

- FedEx International

- UPS Supply Chain Solutions

- Cargolux (specialized electronics)

- Cathay Pacific Cargo

ROAD/TRUCK FREIGHT (Regional - ~10-15% of volume)

European Network:

- Hamburg, Germany → Netherlands/Belgium/France distribution centers

- Manchester, UK → European markets

- Last-mile delivery to automotive tier 1 suppliers (Bosch, Continental)

Asia Network:

- Dongguan → Hong Kong/Shenzhen distribution

- Shanghai → Regional China distribution

- Malaysia/Philippines → Regional ASEAN markets

Characteristics:

- 1-3 day regional delivery

- Temperature-controlled trucks

- Just-in-time delivery to manufacturing customers

RAIL FREIGHT (Emerging - ~5% of volume)

China-Europe Rail Corridor:

- Shanghai/Wuxi → Duisburg/Hamburg via China Railway Express

- Used for: Mid-priority shipments, balancing cost and speed

- Transit time: 14-18 days (faster than ocean, cheaper than air)

SUPPLY CHAIN CHARACTERISTICS BY PRODUCT FLOW

Inbound to Nexperia (Raw Materials)

- Primary Mode: Ocean freight (90%)

- Volume: Silicon wafers, lead frames, chemicals

- Frequency: Scheduled monthly/quarterly deliveries

- Strategy: Just-in-time procurement with safety stock

Inter-Facility Transfers

- Primary Mode: Air freight (60%) + Ocean (40%)

- Volume: Wafers from Germany/UK to China assembly

- Critical Path: Hamburg → Dongguan (most volume)

Outbound from Nexperia (Finished Goods)

- Distribution (56% of revenue): Mixed ocean/air based on inventory levels

- OEM Direct (40% of revenue): Scheduled ocean with air for urgent orders

- EMS Customers (4% of revenue): Primarily just-in-time air freight

CURRENT SUPPLY CHAIN RISKS (As of October 2025)

- Geographic Concentration: 80% of assembly capacity in China (70% in Dongguan alone)

- Export Controls: Chinese export restrictions on Nexperia products imposed

- Geopolitical Tensions: Dutch government control vs Chinese ownership

- Single-Source Dependencies: Limited silicon wafer suppliers

- Customer Concentration: Heavy automotive exposure (62.3% of revenue)

KEY SUPPLY CHAIN METRICS

- Annual Shipment Volume: 100+ billion units

- Lead Time: Standard 8-20 weeks; expedited 4-8 weeks

- Inventory Strategy: Just-in-time with strategic buffers

- Quality Standards: IATF 16949, ISO 9001, ISO 14001, AEC-Q101

- Geographic Revenue: Greater China 48%, EMEA 22%, Americas 9%, Asia-Pacific 21%

%20-%202026-07-17T152701.754.png)

%20-%202026-07-17T104412.520.png)

%20-%202026-07-08T100322.158.png)