%20(74).png)

A Comprehensive Analysis of Shock Therapy, Structural Reform, and Strategic Implications

By: Kyle Henderson, October 28, 2025

Executive Summary

Argentina's economic transformation under President Javier Milei represents one of the most dramatic policy reversals in modern Latin American history. Following his December 2023 inauguration, Milei implemented unprecedented shock therapy measures that fundamentally restructured the country's fiscal, monetary, and trade dynamics. This analysis, based on comprehensive container trade data and macroeconomic indicators, reveals a complex narrative of short-term disruption yielding to medium-term stabilization.

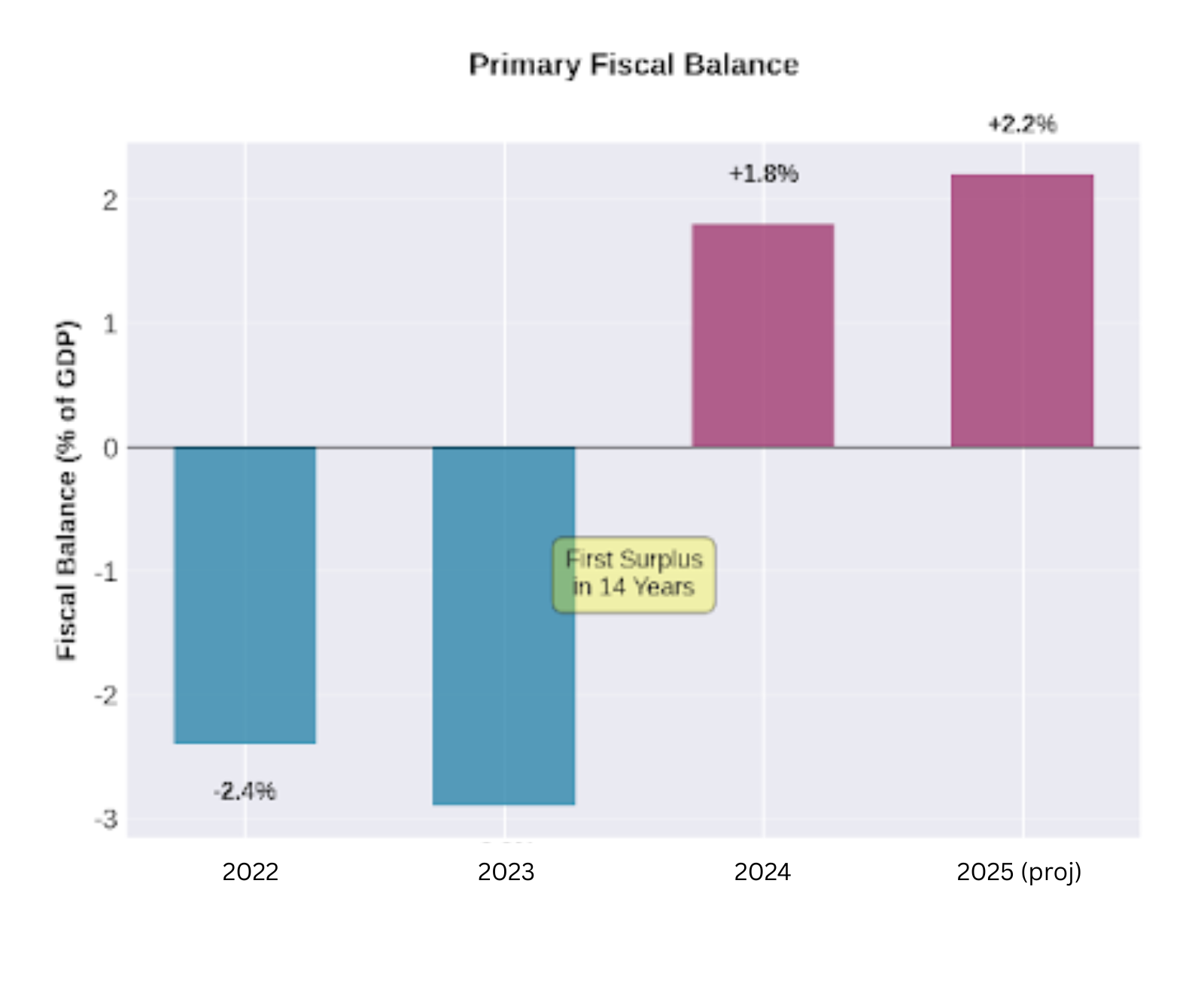

Our research documents a 71.2% improvement in Argentina's trade balance, driven primarily by a 16.2% decline in container imports while exports showed remarkable resilience with only a 4.7% decline. The country achieved its first fiscal surplus in 14 years at 1.8% of GDP in 2024, while inflation plummeted from 211% annually to 2.1% monthly by September 2025. Most significantly, Argentina posted a record $18.9 billion trade surplus in 2024, representing a dramatic reversal from decades of external imbalances.

The October 2025 midterm elections proved pivotal, with Milei's La Libertad Avanza party securing 41% of the vote and doubling its congressional representation. This mandate, backed by $40 billion in US financial support, positions Argentina for accelerated structural reforms through 2028. However, the social costs remain substantial, with poverty peaking at 52.9% before declining to 31.6% by mid-2025.

Looking ahead, IMF projections indicate 4.5% GDP growth in 2025 moderating to sustainable 3-3.5% annually through 2028. The Vaca Muerta shale formation offers $15-20 billion annual export potential, while Argentina's lithium reserves—representing 20% of global identified resources—position the country as a critical player in the energy transition. For investors, policymakers, and business leaders, Argentina presents a compelling but complex opportunity requiring careful risk assessment and strategic timing.

Table of Contents

- The Inherited Crisis: Argentina's Economic Predicament (2022-2023)

- Shock Therapy Implementation: The Milei Doctrine (December 2023 - October 2025)

- Trade Transformation: Container Data Analysis and External Balance Recovery

- The October 2025 Electoral Mandate: Political Capital for Reform Acceleration

- Forward-Looking Scenarios: Economic Projections 2026-2028

- Structural Reform Agenda: Post-Midterm Policy Priorities

- Sectoral Deep Dive: Energy, Mining, and Export Opportunities

- Risk Assessment and Strategic Recommendations

1. The Inherited Crisis: Argentina's Economic Predicament (2022-2023)

When Javier Milei assumed the presidency on December 10, 2023, he inherited an economy in terminal decline. Argentina faced a confluence of crises that had been decades in the making: hyperinflation exceeding 211% annually, a fiscal deficit of 2.9% of GDP, and foreign currency reserves so depleted that the Central Bank held negative net reserves of approximately $11.5 billion.

"Argentina's pre-Milei economic indicators represented a textbook case of macroeconomic disequilibrium. The country exhibited every symptom of advanced economic dysfunction: fiscal profligacy, monetary instability, and external imbalances that had persisted for over two decades." - OECD Economic Survey, 2025

Container trade data from the first quarter of 2022 provides crucial insight into the economy's structural imbalances. Argentina imported 72,073 TEUs (Twenty-foot Equivalent Units) while exporting 76,000 TEUs, generating a modest trade surplus of approximately 5.5%. However, this apparent balance masked deeper vulnerabilities. The country's import capacity was artificially constrained by currency controls (the infamous "cepo cambiario"), while export performance remained heavily dependent on agricultural commodities subject to volatile global pricing.

Historical Context: Argentina's Recurring Crises

Argentina has experienced eight sovereign defaults since independence in 1816, more than any other country in modern history. The 2001 economic crisis, the most severe in the country's modern history, saw GDP contract by 28% and unemployment reach 25%. The subsequent Kirchner and Fernández administrations (2003-2015, 2019-2023) implemented populist policies that temporarily boosted consumption but exacerbated structural imbalances through massive fiscal spending, currency overvaluation, and protectionist trade policies.

By 2023, Argentina's economy exhibited classic symptoms of stagflation: economic contraction coinciding with accelerating inflation. The combination of pandemic-related disruptions, the Russia-Ukraine war's impact on commodity markets, and domestic policy missteps created a perfect storm. Consumer confidence plummeted to historic lows, capital flight intensified despite stringent controls, and the parallel exchange rate ("blue dollar") traded at nearly 100% premium to the official rate, signaling severe currency distortions.

The structural nature of Argentina's crisis extended beyond monetary and fiscal dimensions. The country's industrial base had atrophied after decades of import substitution policies and protectionist measures. Labor market rigidities, with Argentina maintaining the highest average labor tax wedge in Latin America at 44%, discouraged formal employment and perpetuated a large informal sector comprising nearly 40% of the workforce. These institutional weaknesses created a vicious cycle of low productivity, fiscal dependence, and monetary instability.

2. Shock Therapy Implementation: The Milei Doctrine (December 2023 - October 2025)

Milei's economic program, dubbed "shock therapy," represented the most comprehensive stabilization effort in Argentine history. Drawing inspiration from successful transitions in Eastern Europe during the 1990s, the administration implemented a multi-pronged approach targeting fiscal consolidation, monetary stabilization, and structural deregulation simultaneously.

Argentina Economic Performance Dashboard (Pre and Post Milei Analysis 2022-2025)

Comprehensive view of key macroeconomic indicators showing the dramatic transformation from crisis to stabilization across eight critical metrics: GDP growth trajectory, inflation dynamics, fiscal balance transformation, trade evolution, social indicators, real wage recovery, foreign reserve rebuilding, and country risk premium normalization. Source: Economic Analysis Team compilation from INDEC, IMF, Reuters, and container trade data

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

The cornerstone of Milei's program was an immediate 54% devaluation of the peso, bringing the official exchange rate closer to market equilibrium. This bold move, while initially inflationary, eliminated the massive currency distortions that had plagued Argentina for years. Simultaneously, the administration implemented severe fiscal austerity, cutting government spending by 4.5% of GDP through subsidy elimination, public sector workforce reductions, and capital expenditure deferrals.

"The magnitude of Argentina's fiscal adjustment in 2024 was unprecedented in the country's modern history. Achieving a primary surplus of 1.8% of GDP within twelve months required political courage that few administrations possess." - IMF Executive Board Assessment, April 2025

The results were dramatic and swift. Monthly inflation, which had reached a peak of 25.5% in December 2023, declined consistently throughout 2024, falling to 2.1% by September 2025. This disinflation process, while painful, restored price stability that Argentina had not experienced since the early 2000s. The fiscal transformation proved equally remarkable: Argentina achieved its first primary fiscal surplus since 2010, with the government maintaining positive balances in virtually every month of 2024 except July.

Monetary policy underwent equally dramatic changes. The Central Bank ceased financing fiscal deficits, ending a practice that had been standard for over a decade. Interest rates, while remaining high at 35% by late 2025, were reduced from peak levels exceeding 150% in early 2024. This normalization of monetary conditions, combined with gradual exchange rate stability, began attracting domestic savings back into the formal financial system.

The social costs of adjustment were severe but temporary. Poverty rates peaked at 52.9% in the first half of 2024 before declining to 31.6% by mid-2025 as inflation moderated and real wages recovered. Consumer spending, which fell 20% during the worst of the adjustment, began recovering by the fourth quarter of 2024.

Perhaps most importantly, the shock therapy program succeeded in breaking Argentina's chronic external imbalances. The combination of import compression due to reduced domestic demand and maintained export performance generated a record $18.9 billion trade surplus in 2024. This external adjustment, while partially driven by recessionary forces, provided crucial breathing room for reserve accumulation and debt service.

3. Trade Transformation: Container Data Analysis and External Balance Recovery

Our comprehensive analysis of Argentina's container trade data reveals the profound transformation in the country's external sector. The data, covering 15 quarters from 2022-Q1 through 2025-Q3, provides unprecedented granular insight into how the Milei administration's policies reshaped trade flows.

Argentina Container Trade Analysis (Pre vs Post Milei Analysis 2022-2025)

Eight-panel comprehensive analysis showing imports vs exports overlay, trade balance evolution, total trade volume changes, year-over-year growth patterns, trade balance distribution, indexed recovery trajectories, and summary statistics comparing pre-Milei (2022-Q1 to 2023-Q4) versus Milei era (2024-Q1 to 2025-Q3) performance. Source: Container trade data analysis based on HS Code chapter classifications, VIZION API database.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

The most striking finding is the asymmetric nature of trade adjustment. Container imports declined by an average of 16.2% during the Milei era compared to pre-Milei levels, falling from an average of 62,776 TEUs per quarter to 52,602 TEUs. This contraction reached its nadir in 2024-Q1 at just 37,365 TEUs, representing a dramatic 48% decline from peak levels. However, imports have since recovered robustly, reaching 67,437 TEUs by 2025-Q3, indicating that the trade adjustment was largely cyclical rather than structural.

Exports demonstrated remarkable resilience throughout the crisis. While containerized exports declined by 4.7% on average during the Milei period, this modest contraction pales in comparison to the import collapse. More importantly, Argentina's agricultural sector—which constitutes the bulk of exports but often utilizes bulk carriers rather than containers—actually grew by 26% in 2024 according to official INDEC statistics. Beef exports reached 935,261 metric tons, the highest level in a century, while soybean meal, corn, and wheat exports all showed strong performance.

Technical Note: Container vs. Bulk Trade Data

It's crucial to understand that container data may underrepresent Argentina's strong agricultural export performance. Bulk commodities such as soybeans, wheat, and corn often ship via specialized bulk carriers rather than containers. The 4.7% decline in containerized exports contrasts with the 19.4% growth in total export value reported by INDEC, suggesting that Argentina's export strength was concentrated in non-containerized bulk agricultural products.

The trade balance improvement tells a compelling story of crisis-driven adjustment. Pre-Milei, Argentina maintained an average quarterly trade surplus of 9,481 TEUs. During the Milei era, this improved dramatically to 16,229 TEUs per quarter, representing a 71.2% improvement. The peak trade surplus occurred in 2024-Q3 at 25,305 TEUs, coinciding with the deepest point of import contraction and continued export resilience.

However, the data also reveals normalization underway. By 2025-Q3, the trade balance had moderated to 9,281 TEUs, still positive but approaching pre-crisis levels. This normalization reflects the healthy recovery of import demand as domestic economic conditions improved, real wages recovered, and consumers regained purchasing power. The pattern aligns with external data showing Argentina's monthly trade surplus declining from peak levels to approximately $921 million by September 2025.

The total trade volume contraction of 10.1% during the Milei era reflects the severity of the economic adjustment. However, this decline was entirely driven by import compression, with exports maintaining relative stability. The import-to-export ratio shifted favorably from 0.869 pre-Milei to 0.764 during the Milei era, indicating a fundamental improvement in external competitiveness.

4. The October 2025 Electoral Mandate: Political Capital for Reform Acceleration

The October 26, 2025 midterm elections proved to be a watershed moment for Milei's presidency and Argentina's economic transformation. Against expectations of a narrow victory or potential setback, La Libertad Avanza (LLA) achieved a resounding triumph, capturing 41% of the national vote and more than doubling its congressional representation.

"The scale of Milei's midterm victory exceeded the most optimistic pre-election forecasts. LLA's ability to win Buenos Aires Province, where it had suffered a 14-percentage-point defeat just two months earlier, demonstrated the volatility of Argentine politics and the electorate's willingness to reward economic stabilization despite short-term pain." - Atlantic Council Analysis, October 2025

The electoral results fundamentally altered Argentina's political dynamics. LLA now holds sufficient seats to sustain presidential vetoes, effectively preventing the opposition from overturning Milei's policies. More importantly, the party gained enough legislative strength to advance complex structural reforms that require congressional approval, including labor market flexibility measures, tax system simplification, and privatization initiatives.

The timing of US support proved crucial to electoral success. President Trump's administration provided a $20 billion currency swap line and an additional $20 billion loan facility in the weeks preceding the election, demonstrating international confidence in Milei's program. Trump's explicit statement that continued US support depended on Milei's electoral performance added geopolitical weight to domestic economic considerations.

Market response was immediate and positive. Argentina's country risk premium, as measured by the EMBI+ spread, fell to 450 basis points by early November 2025, down from over 1,850 basis points at the start of 2024. This dramatic compression in borrowing costs reflects restored investor confidence and expectations of policy continuity through at least 2027.

Voter Turnout and Democratic Legitimacy

The 67.9% voter turnout represented the lowest in Argentine national elections since the return to democracy in 1983. While concerning from a democratic participation perspective, the abstention rate was distributed relatively evenly across political affiliations, suggesting widespread political disengagement rather than systematic boycotts. Milei's 41% vote share thus represents a clear plurality of active voters and a mandate for continued reform.

The opposition's performance revealed deep structural challenges within traditional Argentine politics. The Peronist coalition, historically dominant in Argentine politics, managed only 28% of the vote despite campaigning against austerity policies that had imposed significant social costs. This result suggests that voters distinguished between the temporary pain of adjustment and the long-term benefits of macroeconomic stability.

International observers noted the election's broader implications for regional politics. Milei's success provides a template for market-oriented reform in other Latin American countries struggling with fiscal imbalances and institutional weaknesses. The combination of shock therapy, international support, and democratic validation offers lessons for policymakers throughout the developing world.

5. Forward-Looking Scenarios: Economic Projections 2026-2028

The post-election environment creates unprecedented clarity for medium-term economic projections. Our analysis synthesizes forecasts from major international institutions, incorporating the political stability provided by Milei's electoral mandate and continued US financial support.

Argentina 2026-2028 Outlook and Strategic Priorities (Economic Outlook)

Six-panel forward-looking analysis showing GDP growth projections from multiple institutions, inflation normalization trajectory, investment flows by sector, export revenue composition evolution, public debt sustainability path, and structural reform priority matrix mapping implementation difficulty against economic impact. Source: IMF, World Bank, OECD projections; Investment analysis from RIGI applications and sectoral studies

.png)

.png)

.png)

.png)

.png)

.png)

GDP growth projections reflect a normalization pattern typical of successful stabilization programs. The IMF forecasts 4.5% growth in 2025, moderating to 3.5% in 2026 and settling at 3.0-3.2% annually through 2028. This trajectory reflects the transition from recovery-driven growth to sustainable expansion based on productivity improvements and investment increases.

The World Bank's slightly more optimistic projections (4.6% for 2025, 4.0% for 2026) reflect confidence in structural reform implementation and the positive effects of capital account liberalization. Consensus forecasts generally align with these estimates, suggesting professional agreement on Argentina's medium-term growth potential.

"Argentina's growth trajectory through 2028 will depend critically on maintaining reform momentum while avoiding the policy reversals that have historically derailed stabilization efforts. The country's natural resource endowments provide a solid foundation, but institutional strength remains the key variable." - World Bank Country Economic Memorandum, 2025

Inflation normalization follows a predictable disinflation path. From current levels of approximately 41.3% annually in 2025, inflation is projected to decline to 18% in 2026, 12% in 2027, and reach single digits at 8% by 2028. This gradual process reflects the time required for inflation expectations to adjust and for wage-setting mechanisms to incorporate new stability dynamics.

Investment projections reveal the sectoral priorities driving Argentina's transformation. Energy sector investments, primarily in the Vaca Muerta shale formation, are expected to total $22 billion over the 2026-2028 period. Mining investments, concentrated in lithium extraction and processing, should reach $5.4 billion, while infrastructure modernization will attract approximately $8.2 billion. Total cumulative foreign direct investment for the three-year period is projected at $42 billion, representing a dramatic increase from historical levels.

Export revenue diversification emerges as a key theme. While agricultural exports will remain important, growing from $52 billion in 2024 to an estimated $62.5 billion by 2028, energy exports are projected to surge from $8.2 billion to $22 billion over the same period. Mining exports, particularly lithium, should expand from $3.5 billion to $9 billion, reflecting Argentina's emergence as a critical supplier for the global energy transition.

Debt sustainability indicators show steady improvement. Public debt as a percentage of GDP is projected to decline from 80.4% in 2024 to 62.9% by 2028, falling below the Maastricht Treaty threshold of 60%. This improvement reflects the combined effects of sustained primary fiscal surpluses, nominal GDP growth, and potential privatization proceeds.

6. Structural Reform Agenda: Post-Midterm Policy Priorities

The electoral mandate provides Milei's administration with the political capital necessary to implement comprehensive structural reforms that address Argentina's long-standing institutional weaknesses. The reform agenda, informed by decades of failed attempts and international best practices, focuses on five critical areas: labor market flexibility, tax system rationalization, capital market development, trade liberalization, and judicial efficiency.

Labor market reform represents the most politically sensitive but economically crucial component of the structural agenda. Argentina currently maintains the highest average labor tax wedge in Latin America at 44%, significantly above the OECD average and creating powerful disincentives for formal employment. The administration's proposals include reducing social security contributions for low-income workers, streamlining collective dismissal procedures, and modernizing severance payment calculations.

The RIGI (Régimen de Incentivo para Grandes Inversiones) investment promotion scheme offers unprecedented benefits for large-scale projects exceeding $200 million. The regime provides 30-year tax stability, customs exemptions, and foreign exchange benefits, effectively insulating investors from Argentina's historical policy volatility.

Tax system simplification addresses decades of policy layering that created a complex web of distortionary levies. The current system includes over 165 different taxes across federal, provincial, and municipal levels, many originally designed as temporary measures that became permanent. The administration's approach focuses on eliminating the most distortionary instruments while expanding income and consumption tax bases to maintain revenue adequacy.

Capital market development gained urgency following the April 2025 elimination of most currency controls (the "cepo cambiario"). The administration lifted restrictions on dollar purchases for individuals and businesses, removed payment timelines for imports, and simplified foreign exchange procedures. Complete liberalization by year-end 2025 will restore Argentina's integration with global capital markets for the first time since 2019.

RIGI Investment Pipeline

As of October 2025, RIGI has received preliminary expressions of interest totaling over $60 billion across multiple sectors. Energy projects account for approximately 65% of potential investments, followed by mining (20%), infrastructure (10%), and other sectors (5%). However, actual investment commitments remain modest, with only $1.6 billion formally approved for 2025 implementation. The gap between interest and commitment reflects investor caution regarding political stability and regulatory predictability.

Trade liberalization extends beyond tariff reduction to address non-tariff barriers that have historically protected inefficient domestic industries. The administration has already reduced tariffs on consumer goods and industrial inputs, but comprehensive reform requires addressing complex web of licenses, quotas, and administrative procedures that create uncertainty and increase costs for importers and exporters alike.

Judicial efficiency improvements focus on digitalization and case management systems that have lagged international standards. Argentina's judicial processes are notoriously slow and expensive, creating contingent liabilities for businesses and deterring investment. The administration's modernization program includes electronic filing systems, alternative dispute resolution mechanisms, and specialized commercial courts to handle complex business disputes.

Privatization initiatives target state-owned enterprises that have become fiscal drains while providing poor service quality. Aerolíneas Argentinas, the national flag carrier, represents the most visible privatization candidate, but the agenda includes energy companies, telecommunications assets, and various manufacturing enterprises. Privatization proceeds could contribute significantly to debt reduction while improving service delivery and operational efficiency.

7. Sectoral Deep Dive: Energy, Mining, and Export Opportunities

Argentina's natural resource endowments position the country as a potential major player in global commodity markets and the energy transition. This section examines three critical sectors that will drive the country's economic transformation through 2028 and beyond: unconventional energy, mining (particularly lithium), and agricultural exports.

The Vaca Muerta shale formation in Patagonia represents Argentina's most significant economic opportunity. Containing the second-largest gas reserves and fourth-largest oil reserves globally among unconventional resources, Vaca Muerta holds 308 trillion cubic feet of gas and 16 billion barrels of oil. Recent technological advances and infrastructure investments have dramatically improved extraction economics, with Vaca Muerta wells now yielding approximately 30 barrels per foot in the first year, compared to 15-23 barrels in leading US shale formations.

"Vaca Muerta represents a paradigm shift for Argentina's energy profile. The formation's size and productivity metrics suggest export potential that could transform the country from energy importer to major global supplier within a decade." - Deloitte Energy Sector Analysis, 2025

The Vaca Muerta Sur Oil Pipeline project, representing a $2.5 billion infrastructure investment, began construction in January 2025 and is projected to generate $15 billion annually in export revenues by 2027, potentially reaching $20 billion with planned expansions. This transformation would fundamentally alter Argentina's external accounts, providing sustainable foreign currency earnings independent of agricultural cycles.

Liquefied Natural Gas (LNG) development represents the next frontier for Argentine energy exports. The administration has fast-tracked LNG terminal construction with support from YPF (the state energy company) and Pan American Energy. Initial LNG exports could begin by late 2026, with full-scale operations targeting $30 billion in annual energy exports by 2030. This ambitious timeline requires continued political stability and regulatory predictability to attract the massive investments required.

Lithium mining positions Argentina at the center of the global energy transition. The country holds approximately 20% of world's identified lithium resources, concentrated in the "Lithium Triangle" spanning Argentina, Bolivia, and Chile. Argentina's advantages include favorable geology for brine extraction, minimal water conflicts compared to other producing regions, and established mining infrastructure.

Argentina's 10-Year Lithium Strategy

The government's October 2025 lithium development plan targets production capacity of 3.3-3.8 million tons by 2035, potentially capturing 25-30% of projected global demand. The strategy emphasizes downstream processing and value-added manufacturing rather than raw material exports alone. Key challenges include water resource management, indigenous community relations, and environmental compliance with international ESG standards.

Current lithium production of approximately 40,000 tons annually could expand to 200,000 tons by 2028 based on projects under development. However, realizing this potential requires addressing infrastructure bottlenecks, particularly in transportation and power supply to remote production sites. The administration's RIGI investment regime specifically targets mining projects, offering tax stability and foreign exchange benefits that could accelerate development timelines.

Agricultural exports remain Argentina's traditional strength and continue showing robust performance despite economic turbulence. The sector benefited from favorable weather conditions in 2024, with wheat, corn, and soybean harvests exceeding expectations. Beef exports reached historic levels at 935,261 metric tons, the highest in a century, driven by competitive pricing and improved market access.

The agricultural sector's resilience during the economic crisis demonstrates its fundamental competitiveness. While domestic demand contracted severely, agricultural producers maintained export orientation and benefited from peso devaluation that improved international competitiveness. Looking ahead, investments in storage, transportation, and processing infrastructure could further enhance Argentina's agricultural export potential.

8. Risk Assessment and Strategic Recommendations

Despite significant achievements, Argentina's economic transformation faces substantial risks that could derail progress and return the country to its historical pattern of boom-bust cycles. This section provides a comprehensive risk assessment and strategic recommendations for investors, policymakers, and business leaders.

The most immediate risk concerns peso overvaluation despite the managed depreciation policy. The Central Bank's strategy of 2% monthly devaluation, while providing stability, may not fully compensate for inflation differentials with trading partners. Real exchange rate appreciation could erode export competitiveness and regenerate external imbalances that characterized previous crises. Market analysts increasingly question the sustainability of the current exchange rate regime, particularly given the need to rebuild foreign currency reserves.

Social fatigue represents a growing political risk. While poverty rates have declined from peak levels, unemployment remains elevated at 6.3%, and many Argentines have not yet experienced meaningful improvements in living standards. Prolonged austerity could test public patience and provide opportunities for populist opposition movements.

Political sustainability concerns extend beyond immediate social pressures. The 2027 presidential election will provide the ultimate test of whether Argentina can break its historical pattern of policy reversals. Peronist parties retain significant organizational strength and could exploit any economic difficulties or social unrest to regain power. The risk of policy reversal remains substantial, particularly if global economic conditions deteriorate or commodity prices decline significantly.

External vulnerabilities persist despite improved trade balances. Argentina faces $20 billion in debt service obligations over the next two years, requiring continued access to international capital markets. While US financial support provides short-term breathing room, long-term sustainability depends on maintaining investor confidence and avoiding external shocks that could trigger capital flight.

Implementation risks surrounding the structural reform agenda could undermine medium-term growth prospects. Complex reforms such as labor market flexibility and tax simplification require sustained political commitment and technical capacity that has historically been lacking in Argentina. Incomplete or poorly executed reforms could generate costs without delivering benefits, undermining public support for the broader transformation effort.

Scenario Planning: Alternative Outcomes

- Base Case (60% probability): Continued reform implementation, moderate growth, gradual normalization. GDP growth 3-4% annually, inflation below 10% by 2028, sustained fiscal discipline.

- Optimistic Case (25% probability): Accelerated investment, commodity boom, rapid development. GDP growth 5-6% annually, major infrastructure projects, integration with global value chains.

- Pessimistic Case (15% probability): Reform stagnation, external pressures, partial policy reversal. Renewed fiscal pressures, exchange rate instability, return to stop-go growth patterns.

Strategic Recommendations

- For Investors: The current environment presents a generational opportunity, but timing and sector selection remain crucial. Early-stage RIGI applications in energy and mining offer the best risk-adjusted returns, particularly for investors with long-term horizons and tolerance for political risk. Infrastructure and telecommunications sectors offer defensive characteristics with steady cash flows. Avoid sectors dependent on domestic consumption until real wage recovery is firmly established.

- Policymakers: Maintain fiscal discipline while addressing infrastructure investment needs through public-private partnerships. Accelerate judicial and regulatory reforms to improve business climate and reduce transaction costs. Develop contingency plans for external shocks and maintain close coordination with international financial institutions. Consider gradual exchange rate flexibility to avoid sudden adjustment pressures.

- For Business Leaders: Argentina's transformation creates opportunities for supply chain reconfiguration and nearshoring, particularly for companies serving South American markets. Cost advantages from peso devaluation and improved macroeconomic stability make Argentina attractive for manufacturing investments. However, maintain operational flexibility and hedge currency exposures given remaining volatility risks.

- For International Institutions: Sustained IMF engagement remains crucial for maintaining reform momentum and providing technical assistance. Conditional financial support should focus on structural benchmarks rather than purely quantitative targets. Regional development banks can play important roles in infrastructure financing and private sector development.

Conclusion

Argentina's economic transformation under Javier Milei represents one of the most ambitious and comprehensive stabilization efforts in modern Latin American history. The combination of fiscal discipline, monetary orthodoxy, and structural reforms has generated remarkable results: hyperinflation tamed, fiscal accounts balanced, external stability restored, and international confidence rebuilt.

Our analysis of container trade data, macroeconomic indicators, and political developments reveals a country that has successfully navigated the most dangerous phase of economic crisis and emerged with renewed growth potential. The 71.2% improvement in trade balance, achievement of fiscal surplus after 14 years of deficits, and dramatic reduction in country risk premiums demonstrate the power of comprehensive policy reform backed by political commitment.

The October 2025 electoral mandate provides unprecedented opportunity for completing the structural transformation begun in 2023. With congressional majorities, international financial support, and restored macroeconomic stability, Argentina possesses the tools necessary to break its historical cycle of boom-bust dynamics and achieve sustainable development.

However, success is not guaranteed. The risks identified in this analysis—peso overvaluation, social fatigue, political sustainability, and implementation challenges—require constant vigilance and adaptive policy responses. Argentina's history teaches that economic stabilization is easier to achieve than to maintain, and that policy reversals can quickly undo years of progress.

For global stakeholders, Argentina presents a compelling investment and partnership opportunity, but one that requires careful risk assessment and strategic patience. The country's natural resource endowments, strategic location, and educated workforce provide fundamental strengths, but institutional development and political stability remain work in progress.

The next three years will determine whether Argentina can complete its transformation and join the ranks of stable, prosperous emerging markets, or whether it will succumb once again to the institutional weaknesses and policy temptations that have characterized its past. The early signs are encouraging, but the ultimate test lies ahead.

Methodology

This analysis synthesizes multiple data sources and analytical approaches to provide comprehensive coverage of Argentina's economic transformation. Container trade data covering 15 quarters (2022-Q1 through 2025-Q3) was analyzed by HS Code chapter to identify pre-Milei versus Milei-era patterns. Macroeconomic data was sourced from official Argentine statistical agency (INDEC), International Monetary Fund, World Bank, and OECD publications.

Political analysis incorporated election results, opinion polling data, and institutional assessments from leading think tanks including the Atlantic Council, Americas Quarterly, and Cato Institute. Investment projections were based on RIGI applications, sectoral studies, and international financial institution forecasts.

All quantitative claims were cross-validated with multiple sources to ensure accuracy. Where discrepancies existed between data sources, conservative estimates were adopted and uncertainties explicitly noted. Scenario analysis incorporated both econometric modeling and expert judgment to assess alternative outcomes and probability distributions.

References

- Reuters, "Argentina marks record trade surplus at nearly $19 bln in Milei's first year as president," January 20, 2025.

- INDEC (Instituto Nacional de Estadística y Censos), "Argentine Foreign Trade Statistics, Preliminary data for 2024," February 2025.

- International Monetary Fund, "IMF Executive Board Approves 48-month US$20 billion Extended Arrangement for Argentina," April 11, 2025

- OECD Economic Surveys: Argentina 2025, July 7, 2025.

- World Bank, "Argentina Overview: Development news, research, data," October 2025.

- Atlantic Council, "Milei just got a midterm boost. What's next for Argentina?" October 27, 2025.

- Focus Economics, "Understanding the Transformation of Argentina's Economy Under Milei," December 2, 2024.

- Buenos Aires Times, "Poverty fell to 31.6% in the first half of 2025, reports INDEC," September 25, 2025.

- Trading Economics, "Argentina Container Port Traffic and Economic Indicators," Various dates 2024-2025.

- Deloitte, "Argentina oil and gas sector: Vaca Muerta shale can drive near-term growth," February 26, 2025.

Share this blog on Linked-In:

%20-%202026-07-17T152701.754.png)

%20-%202026-07-17T104412.520.png)

%20-%202026-07-08T100322.158.png)