El Niño Déjà Vu? Why This Cycle's Booking Curve Looks Different

When an El Niño cycle returns, the instinct is to expect history to rhyme. Our booking data says it doesn't, at least not cleanly. Comparing the last El Niño window (2023-W22 to 2024-W18) against the current cycle (2025-W22 to 2026-W18), the calendar-driven swings look nearly identical, but the trajectory of demand has a visibly different shape. That tension, familiar seasonality paired with an unfamiliar curve, is the real story.

Booking volume is an early signal. It moves weeks before cargo does, which makes it useful for spotting inflection points while there's still time to act. Below, we walk through five major lanes, compare the two cycles week-for-week, and separate what's seasonal from what's genuinely changed. We avoid overstating cause: El Niño is, at most, one of several overlapping factors alongside tariffs, freight rates, capacity decisions, and ordinary seasonality.

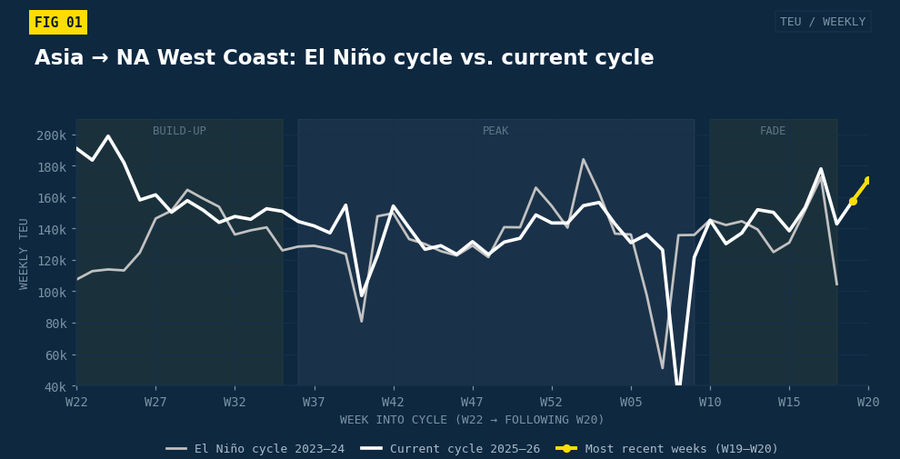

The headline: this cycle starts hotter, then eases

The Asia to North America West Coast lane is the volume backbone of the trans-Pacific, so it's the clearest place to see the difference in shape. Aligning both cycles on "weeks into the cycle," the current period opens well above the last El Niño cycle, then converges and softens through the peak window. The two most recent weeks (2026-W19 and W20) tick back up. These bookings have already been made, and only the arrivals are still ahead, so they're observed data rather than a forecast, though just two weeks of it.

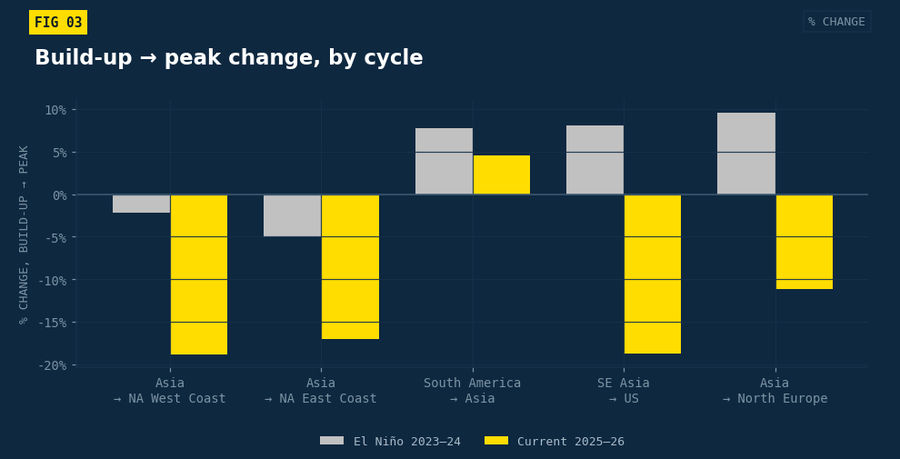

That "hot early, soft into peak" pattern is the opposite of what we saw last time. In 2023 to 2024 the West Coast lane was essentially flat from build-up to peak (−2%); this cycle it fell −19% across the same transition. A curve that front-loads and then fades reads more like demand pulled forward in the calendar than demand building through the season, a pattern consistent with front-loading ahead of tariff or rate deadlines rather than something weather alone would produce.

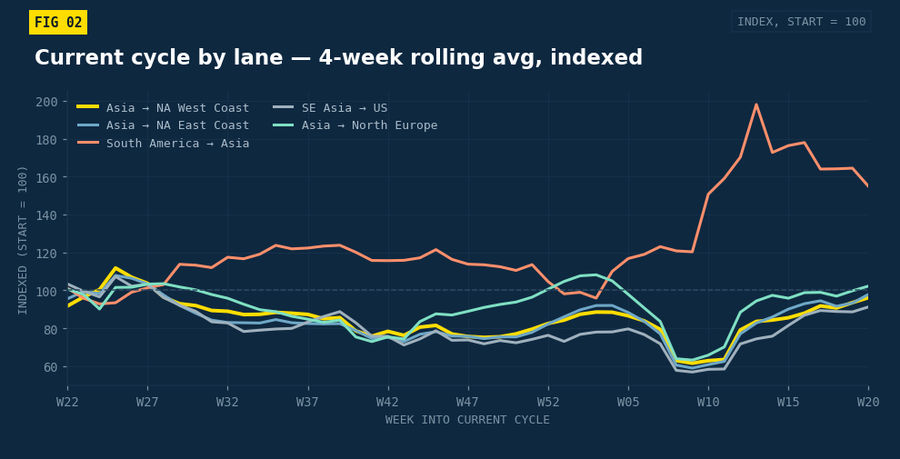

All five lanes, on one axis

Lanes differ enormously in size. North Europe books over 180,000 TEU in a typical week while South America to Asia books under 30,000, so to compare their shape we index each lane's 4-week rolling average to its own starting level.

Did bookings accelerate into the peak?

This is the question that most directly tests the "El Niño déjà vu" idea. Last cycle, four of five lanes built upward into the peak window. This cycle, most of them decelerated into it. The reversal is sharpest on the trans-Pacific and Southeast Asia lanes.

The acceleration that defined the last cycle didn't reappear. Four of five lanes that built into the peak in 2023 to 2024 decelerated into it this time.

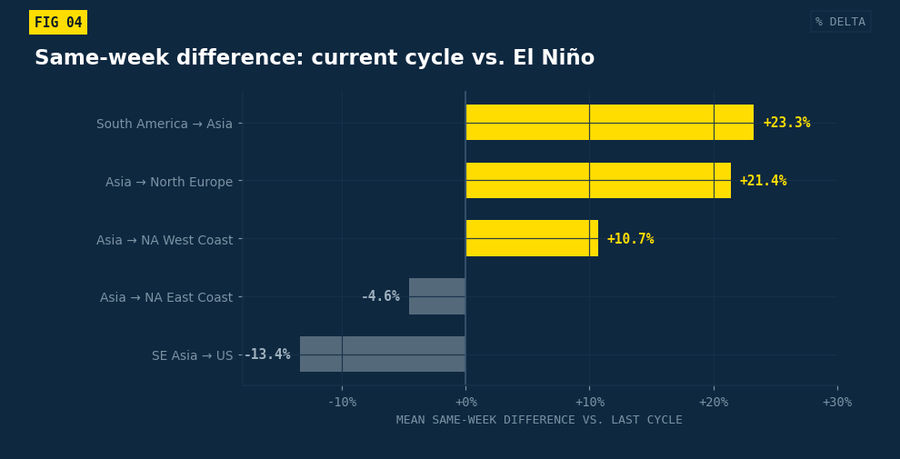

Hotter or cooler? The same-week read

The cleanest single metric is the same-week comparison: line up matching calendar weeks across the two year-pairs and ask whether the current cycle is running above or below the last one. Three lanes are clearly hotter; two are clearly cooler.

South America to Asia (+23%) and Asia to North Europe (+21%) lead; Asia to NA East Coast (−5%) and SE Asia to US (−13%) trail. Notably, the SE Asia to US weakness runs against the popular "China + 1" sourcing-shift narrative within this window, worth a closer look before reading too much into it.

The crucial caveat: it's the calendar, not the climate

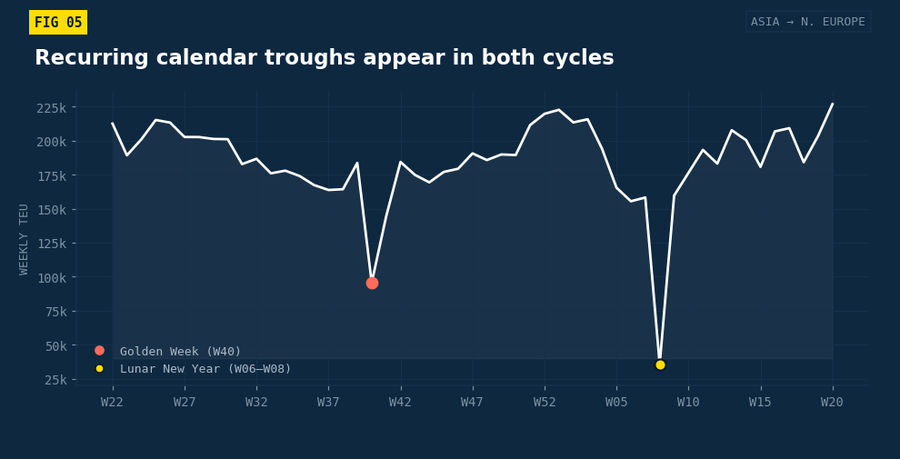

Before attributing anything to El Niño, look at what actually drives the biggest week-to-week swings. They cluster at Golden Week (W40) and Lunar New Year (W06 to W08), and they appear in both cycles on every China-origin lane. On Asia to North Europe, Golden Week alone cuts bookings 44 to 46% below neighboring weeks, in both periods.

The control-lane test: South America to Asia doesn't follow the Chinese factory calendar, and sure enough, it shows almost no Golden Week dip (just −4% to −10% versus −31% to −46% on China-origin lanes). That contrast is strong evidence the big swings are seasonal mechanics, not an El Niño signal.

Reading the full picture

The table below brings the lanes together: average weekly bookings in each cycle, the full-cycle change, the same-week read, and a plain-language interpretation.

So what's seasonal, what's demand, and what's disruption?

Clearly seasonal: the W40 and W06 to W08 troughs, recurring on every China-origin lane in both cycles. Likely structural or demand-driven: South America to Asia growth (+21%), driven by commodity and agricultural flows on a different calendar. Likely disruption- or policy-related: the trans-Pacific deceleration into the peak, consistent with front-loading. And entangled with routing: North Europe's strength, where Red Sea diversions can inflate booked TEU independent of underlying demand.

The takeaway

If you came expecting a re-run of the last El Niño, the data resists that framing. The seasonal mechanics rhyme, the same Golden Week and Lunar New Year troughs in the same weeks, but the demand curve has shifted: hotter early on the trans-Pacific, cooler on Southeast Asia, and structurally stronger on South America to Asia and North Europe. The most defensible read is that bookings moved, and that several forces (tariffs, rates, capacity, rerouting, and seasonality) are more likely behind it than weather alone.

Method and caveats: Weekly booked TEU by lane (VIZION TradeView); 100 weeks per lane across five lanes. The same-week comparison aligns matching ISO weeks across the two year-pairs; rolling figures use a 4-week trailing average. The two most recent weeks (2026-W19 and W20) are observed bookings whose shipments arrive later; with only two weeks they are directional, not a trend. Booked TEU can differ from loaded volume, and a few outlier weeks sit at the edge of normal seasonality. El Niño is treated as one possible contributing factor among several, not an established cause.

%20-%202026-07-02T085236.864.png)

.png)

%20-%202026-06-30T153212.809.png)